Meta Description:

Trying to choose between a personal loan or a credit card? Learn the key differences, pros and cons, and which option is better for your financial goals.

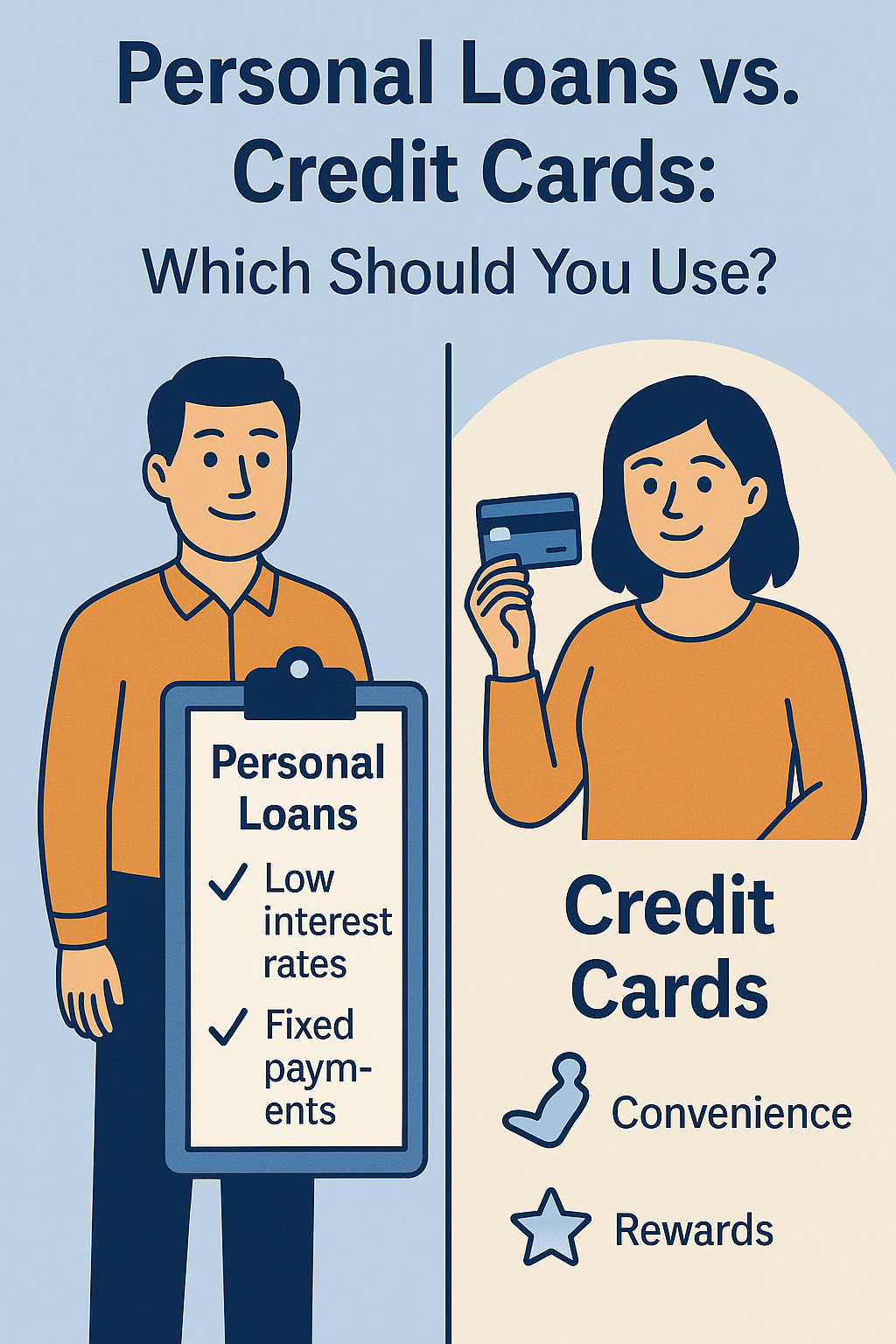

💳 Personal Loan or Credit Card? Here’s How to Decide

When you need access to money—whether for an emergency, a large purchase, or paying off debt—you’ll likely find yourself choosing between two common options: a personal loan or a credit card.

Both can be useful, but they work very differently and can impact your finances in very different ways. In this blog, we’ll break down the pros, cons, and best uses for each to help you make the smartest choice for your situation in 2025.

📌 Quick Comparison

| Feature | Personal Loan | Credit Card |

|---|---|---|

| Type | Installment Loan | Revolving Credit |

| Interest Rates | Fixed (6%–36%) | Variable (17%+ average in 2025) |

| Repayment Term | 1–7 years (fixed payments) | Ongoing (minimum required) |

| Access to Funds | Lump sum | Ongoing credit limit |

| Credit Score Impact | Helps with regular payments | Can hurt with high balances |

| Best For | Large one-time expenses, debt consolidation | Smaller, ongoing expenses |

💰 What Is a Personal Loan?

A personal loan is a type of installment loan you borrow from a bank, credit union, or online lender. You get a lump sum of money upfront and repay it over a set period of time with fixed monthly payments.

Pros:

-

Lower interest rates than credit cards (especially with good credit)

-

Predictable payments and payoff date

-

Great for debt consolidation or big purchases (like medical bills, moving costs, or home repairs)

Cons:

-

You may need good to excellent credit to qualify for low rates

-

You can’t borrow more later—you get one lump sum

-

Fees may apply (origination fees, prepayment penalties)

💳 What Is a Credit Card?

A credit card is a revolving line of credit. You can borrow as needed up to your credit limit and pay it back over time. Minimum payments are required each month, but interest charges apply to carried balances.

Pros:

-

Instant access to funds (swipe or tap anytime)

-

Great for short-term or emergency expenses

-

Can earn rewards or cash back

-

No interest if you pay the balance in full each month

Cons:

-

High interest rates (often 17%–30%)

-

Easy to overspend

-

Carrying a balance long-term can hurt your credit

-

Only minimum payments? You could stay in debt for years

🤔 When Should You Use a Personal Loan?

A personal loan is typically better when:

-

You’re consolidating high-interest credit card debt

-

You have a large one-time expense (wedding, funeral, dental work, etc.)

-

You want fixed monthly payments and a clear payoff plan

-

You qualify for a lower interest rate than your credit cards offer

📌 Example: You owe $10,000 on 3 credit cards at 23% interest. A personal loan at 10% saves you hundreds—and gives you a structured way to pay it off in 3 years.

🤔 When Should You Use a Credit Card?

A credit card makes more sense when:

-

You’re making small, manageable purchases you can repay quickly

-

You want to build or improve your credit score

-

You need flexibility and don’t want to commit to a loan

-

You plan to pay off the balance in full every month

📌 Example: You have a $300 car repair or an unexpected prescription bill. Charging it to your credit card and paying it off next payday makes sense.

⚠️ Warning: Don’t Use a Credit Card for Large Purchases You Can’t Afford

Unless you’re using a 0% APR promotional card, large balances can snowball into long-term, high-interest debt. Personal loans are often a safer and cheaper option in these cases.

📈 What About Your Credit Score?

Both personal loans and credit cards affect your credit—here’s how:

✅ Personal Loans:

-

Boost your score with on-time payments

-

Improve your credit mix (installment + revolving)

-

May lower your score slightly when you first apply

✅ Credit Cards:

-

Help build credit with regular, low utilization

-

High balances hurt your score

-

Late payments can be devastating

🧠 Final Thoughts: Choose Based on Your Purpose

There’s no one-size-fits-all answer—but there is a right tool for the job.

Use a personal loan if:

-

You have a big expense or want to consolidate debt

-

You want lower interest and fixed payments

-

You need financial structure and discipline

Use a credit card if:

-

You can pay it off quickly

-

You’re earning rewards responsibly

-

You need flexible, short-term access to credit

💬 Need help choosing the best personal loan or credit card for your situation?

Drop your question below or message me for a personalized breakdown—no pressure, just smart money help.